Credit scores are up over the past five years at the national level as well as in every U.S. state and metropolitan area, according to a new review of anonymized and aggregated Experian data. From 2019 to 2024, the average FICO® Score in the U.S. increased from 703 to 715, and also increased for each of the 50 states over the same period.

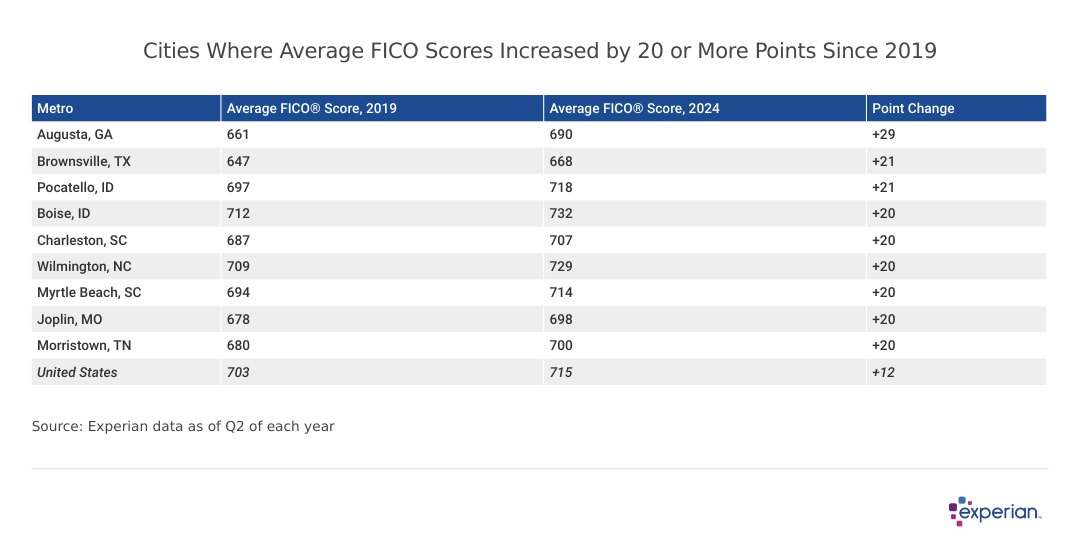

Not one of the more than 400 metro areas observed in this data shows any decline in average FICO Scores since 2019; the smallest gain was four points. However, there are a handful of metros, both large and small, that have seen average FICO Scores increase by 20 points or more over this period.

Mid-sized metros in Southern states make up the majority of the 20-plus point increase club. Many of these cities are attracting newer residents seeking more affordable and available homes for purchase, and construction data indicates that much of the new housing stock in the U.S. is being built in similar metros. Presumably, those with both the means and the credit to purchase homes in what is still broadly a seller's market may be responsible for yanking up average scores significantly more than the national average.

A similar phenomenon may also be occurring in Idaho, where two metros saw average FICO Scores increase by 20 points, thanks in part to in-migration of about 50,000 new residents from neighboring Pacific states annually, according to Census data.

In addition, cities where FICO Scores grew the most over the past five years had more room to improve than other metros: In 2019, only two of the nine cities—Boise, Idaho, and Wilmington, North Carolina—sported average FICO Scores that were above the then-nationwide average FICO Score of 703.

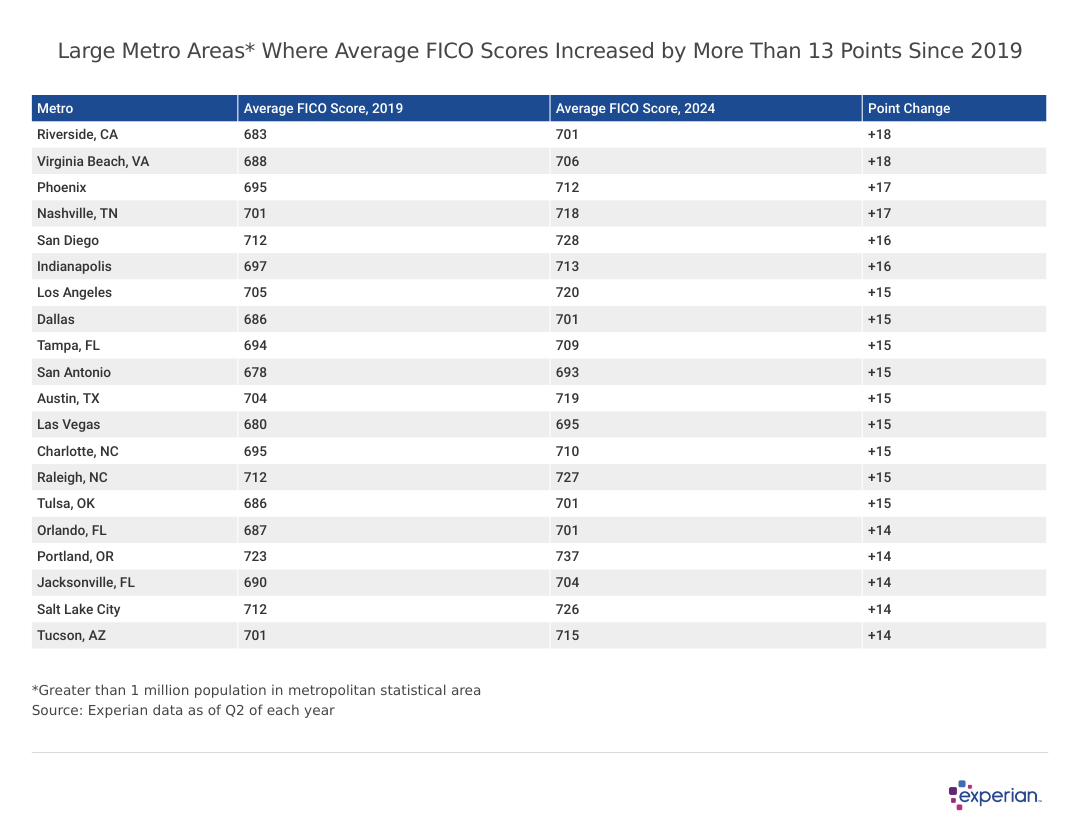

While no large metro grew by 20 points or more over that same period, many did surpass the 13-point average increase. The biggest jumps were in large metros adjacent to even larger metros—Los Angeles neighbor Riverside, California, and D.C.-adjacent Virginia Beach, Virginia, for example, which suggests that some in-migration may be responsible for some of the smaller-city increases.

But even relatively isolated large metros like Salt Lake City and Tulsa, Oklahoma, are also seeing healthy increases in average FICO Scores.

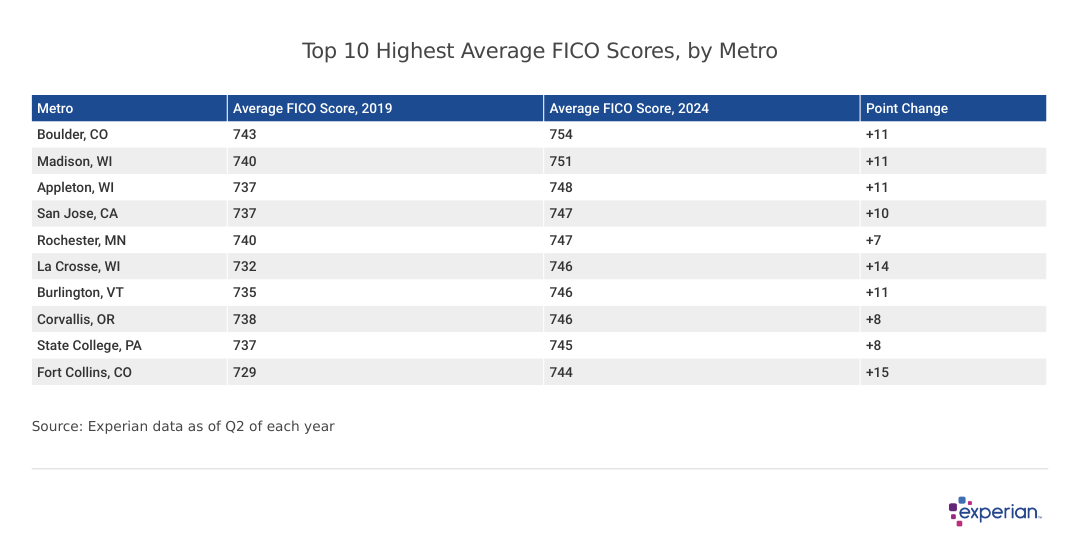

No matter where you live, credit scores are reliant on the same key factors, including payment history, credit utilization, and the length of your credit history. The cities listed below have clearly demonstrated themselves in those regards, reaching an average credit score as much as 39 points above the national average.

The top 10 metros with the highest average FICO Scores are diverse, but they do hold some similarities:

Population factors that can vary greatly by region such as income, employment status, and age might affect someone's ability to manage their finances, but are not listed on a consumer credit report or included in credit score calculations.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include the use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.